RBI digital lending rules explained in simple terms. Learn how loan apps work, risks, safety tips, and fintech regulations in India.

A Simple Question

Have you ever taken a loan from a mobile app within minutes and wondered…

👉 “Is this really safe?”

In recent years, thousands of Indians have experienced both ease and risk while using digital loan apps.

And because of this, something big was done.

Table of Contents

📌 Introduction: Why It Matters

Over the past decade, the way loans are taken in India has been completely transformed.

- Long bank queues → replaced by mobile apps

- Paperwork → replaced by instant approvals

- Days of waiting → replaced by minutes

But along with convenience, serious problems were also created.

👉 This is where RBI digital lending rules were introduced.

These rules were designed to:

- Protect users

- Regulate fintech startups

- Bring transparency to digital lending

📖 The Rise of Digital Lending in India (Context)

A massive shift has been observed in how credit is accessed in India.

👉 According to NITI Aayog, millions of Indians previously lacked access to formal credit systems.

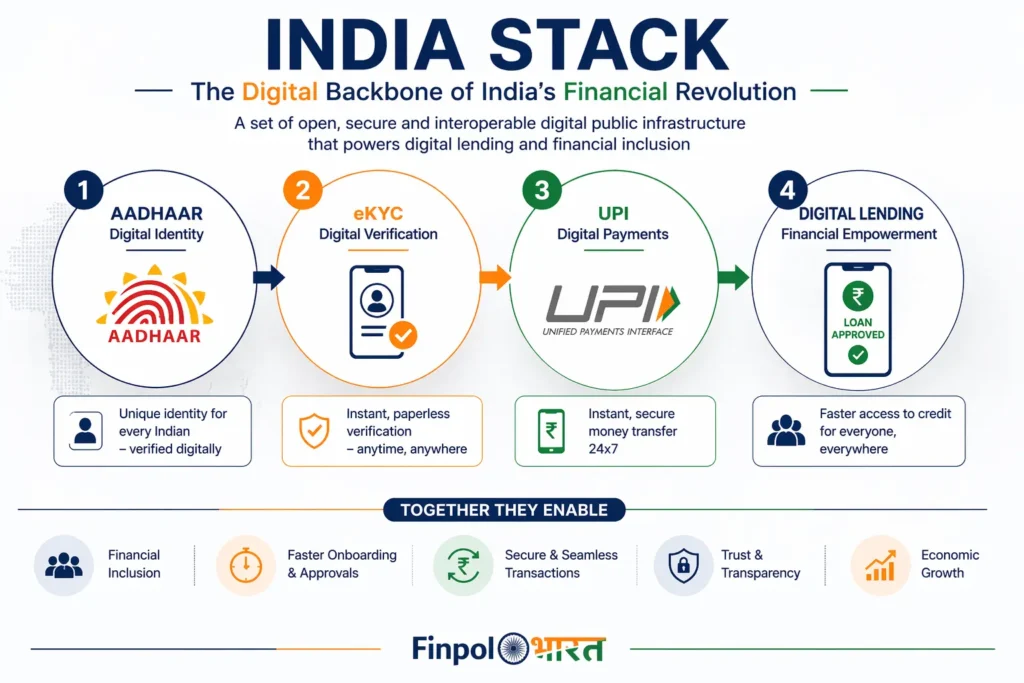

🔧 What Enabled This Growth?

Several powerful systems were built:

- Aadhaar → Digital identity

👉 Learn more: https://uidai.gov.in - eKYC → Instant verification

👉 Explained by Reserve Bank of India: https://www.rbi.org.in - UPI → Fast money transfer

👉 Official site: https://www.npci.org.in/what-we-do/upi/product-overview

👉 Together, these created India’s digital financial backbone.

📊 What Changed in Lending?

Traditional credit systems were gradually replaced by:

- AI-based credit scoring

- Alternative data usage

- App-based loan approvals

As a result:

- Millions of people got access to credit

- Even those without credit history were included

👉 Industry insights:

https://www.bcg.com/publications/india-fintech-report

🚀 Rise of Fintech Startups

A new generation of startups entered the market.

Instead of lending directly, they:

- Partnered with banks/NBFCs

- Provided user interface

- Handled customer acquisition

👉 Industry overview:

https://ficci.in/sector-details/74

This model allowed:

- Fast scaling

- Lower regulatory burden

💡 Why Digital Lending Became Popular

The appeal was simple:

- Loans approved in minutes

- No paperwork

- Easy access for young users

Popular products included:

- Personal loan apps

- Buy Now Pay Later (BNPL)

- Small-ticket instant loans

👉 BNPL explained:

https://www.investopedia.com/buy-now-pay-later-5182291

⚠️ The Dark Side of Digital Lending

As growth increased, problems were also noticed.

❌ Lack of Transparency

- Hidden charges

- Confusing loan terms

- High interest rates

📱 Data Privacy Issues

- Apps accessing contacts & data

- Users unaware of permissions

- Data misuse cases reported

👉 Data protection insights:

https://www.meity.gov.in

🚨 Harassment & Recovery Issues

- Aggressive recovery calls

- Threats & pressure tactics

- Public shaming in extreme cases

👉 Consumer complaints reference:

https://www.rbi.org.in/Scripts/Complaint.aspx

🌍 Foreign-Controlled Apps

- Some apps operated from outside India

- Regulatory control became difficult

👉 News reference:

https://www.thehindu.com/business

👉 Hundreds of such apps were eventually removed.

📈 Growth vs Risk: A Double-Edged Sword

Despite problems, benefits were significant:

✅ Benefits

- Financial inclusion increased

- Small businesses got quick loans

- Rural users gained access

👉 Financial inclusion data:

https://www.worldbank.org/en/topic/financialinclusion

⚠️ Risks

- Over-borrowing

- High default rates

- Lack of awareness

🦠 Pandemic Boost

During COVID-19:

- Demand for loans increased

- Digital lending grew rapidly

- People depended more on apps

👉 Pandemic impact report:

https://www.mckinsey.com/industries/financial-services

But this also exposed:

- Weak lending models

- Risky borrower behavior

💰 Investor Perspective

Fintech saw huge funding:

- High growth expectations

- Rapid startup expansion

👉 Funding trends:

https://www.cbinsights.com/research/report/fintech-trends

But later:

- Funding slowed down

- Profitability concerns increased

🏛️ Why RBI Had to Intervene

A major gap was observed:

👉 Technology was growing faster than regulation

Problems included:

- No clear rules

- Weak consumer protection

- Lack of accountability

👉 Official RBI guidelines:

https://www.rbi.org.in/Scripts/BS_ViewMasDirections.aspx

So, RBI digital lending rules were introduced.

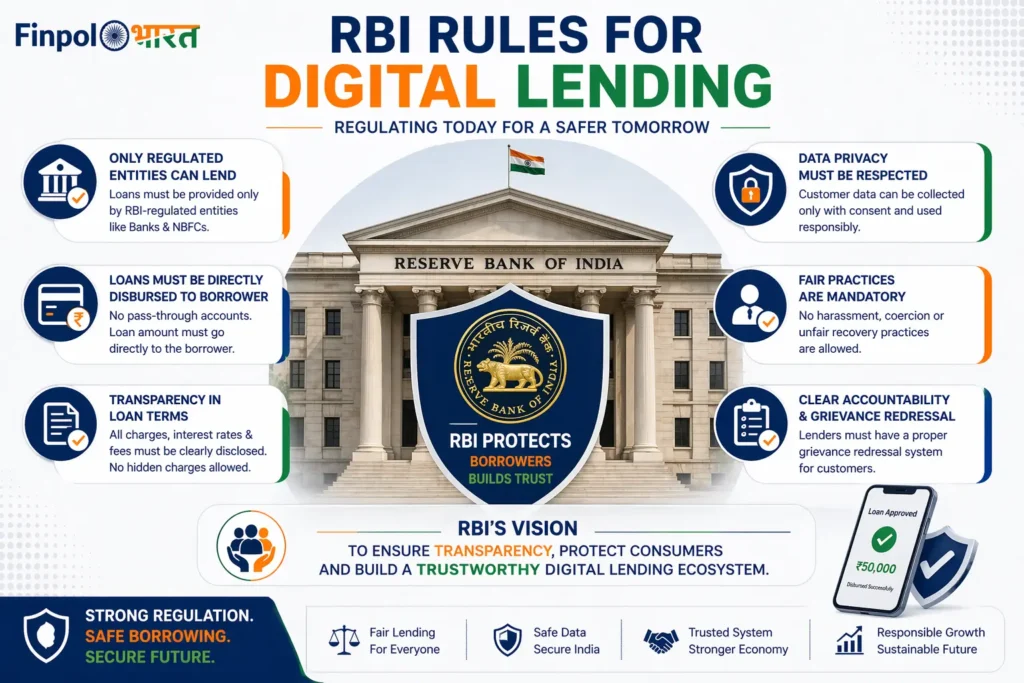

📜 What Are RBI Digital Lending Rules?

These rules were created to:

- Protect borrowers

- Regulate fintech startups

- Ensure transparency

📌 Key Highlights

- Loans must be directly disbursed to borrower

- No hidden charges allowed

- Data privacy must be respected

- Only regulated entities can lend

👉 Full RBI circular:

https://www.rbi.org.in/Scripts/NotificationUser.aspx

👨💼 Real-Life Example

Imagine:

Rahul downloads a loan app and takes ₹10,000.

Earlier:

- Hidden fees were added

- Contacts were accessed

- Harassment risk existed

Now (after RBI rules):

- Full cost is disclosed

- Data access is limited

- Clear accountability is defined

🎯 Benefits for Beginners

For users:

- Safer borrowing

- Transparent pricing

- Reduced fraud risk

For startups:

- Clear compliance framework

- Long-term trust building

⚠️ Challenges & Risks

Even after rules:

- Awareness is still low

- Illegal apps still exist

- Over-regulation concerns

For startups:

- Compliance cost increased

- Innovation slowed in some areas

🛠️ Actionable Tips for Users

Before taking a loan:

- ✅ Check if app is RBI-compliant

- ✅ Read all charges carefully

- ✅ Avoid giving unnecessary permissions

- ✅ Borrow only what you need

👉 RBI awareness page:

https://www.rbi.org.in/financialeducation

🔮 Future of Digital Lending in India

The future will likely be:

- More regulated

- More transparent

- More trust-driven

Trends to watch:

- AI-based lending

- Open banking

- Account Aggregator system

👉 AA framework:

https://sahamati.org.in

🏁 Conclusion + CTA

Digital lending in India has evolved rapidly.

But with growth, risks were also created.

👉 That is why RBI digital lending rules have become essential.

They are not just restrictions —

they are a foundation for a safer fintech future.

🚀 Final Thought

👉 The future of lending will not be about speed — it will be about trust.

india’s Rising Debt Economy is reshaping growth and risk. Is rising borrowing fueling progress or creating a financial time bomb for the future? for more details Click Here